President Trump’s protectionist trade measures against China and other external partners have not caused a reduction of the total US trade deficit. The latter actually grew further as China’s exports found indirect ways into the US and massive domestic spending schemes were expanded during the pandemic.

Almost three years after the Trump administration unleashed the trade war on China, hostilities have not ended, but only entered a truce with the Phase One trade deal signed in January 2020. The US tariff hike on more than $360 billion of Chinese goods has remained in place until today. Washington imposed four rounds of tariffs in 2018 and 2019, with the bulk of the tariffs ranging from 10 to 25 percent coming into force in September 2018 and September 2019. Beijing has gradually retaliated with tariffs ranging from 5 to 25 percent on about $110 billion of US products. The difference in the volumes of products targeted by tariffs reflects the unbalanced bilateral trade.

The covid-19 pandemic took the trade war off the headlines, but its economic disruptions prevented China from meeting the condition of the Phase One deal to purchase an additional $200 billion of US products over the 2017 level. Recently China has approached the Biden administration trying to restart trade discussions, but it seems unlikely that Biden’s policy on China would deviate significantly from his predecessor’s. As a matter of fact, Biden’s trade agenda still underlines that “China’s coercive and unfair trade practices harm American workers, threaten our technological edge, weaken our supply chain resiliency, and undermine our national interests.” In addition, the tech war continues, as top Chinese tech companies suspected to be affiliated with the military remain blacklisted and recently the US Senate passed a bill providing $250 billion in subsides to high-tech sectors competing with China. But Trump’s protectionist agenda does not seem to have reached its target, so why continue it?

The US Trade Deficit Continued Growing

The sharp increase in US tariffs on Chinese goods led to a significant decline in the bilateral trade deficit of about 25 percent, or $108 billion, from 2018 to 2020. Despite the retrenchment of the deficit with China, the US trade deficit in goods with the world has actually increased by around $35 billion from 2018 to 2020, to a record-high $915 billion (graph 1). If Trump’s protectionist measures1 appear to have worked with China, they have certainly not reduced the overall trade deficit. The situation worsened in the first quarter of 2021, when the trade deficit widened by almost 50 percent with China and by more than one-third with the world during the same period in 2020 (US Census Bureau). At the same time, the surplus in the balance of services has shrunk by about 20 percent and it seems that the US is heading for a record-high current account deficit in 2021.

Graph 1: US Trade Deficit with China and the World, 2002–20

Source: US Census Bureau

Chinese Exports Found an Indirect Way to the US

While the US trade deficit with China was shrinking, its deficit with other Asian economies was expanding almost in lockstep. From 2018 to 2020, the US trade deficit in goods to China declined by around $108 billion, but expanded by about $90 billion with Vietnam, Taiwan, Hong Kong, Singapore, Korea, Malaysia, and Thailand. Many analysts interpreted this evolution as a readjustment of global value chains and offshoring of production from China to Vietnam, Taiwan, and other Asian peers. Yet the data points to something else. As US imports from other Asian countries grew by about $32 billion in 2019 and another $30 billion in 2020, China’s exports to the same Asian economies2 grew almost in lockstep (graph 2).

Graph 2: US Imports from and Chinese Exports to Asian Economies, 2018–20

Source: US Census Bureau and UN Comtrade Database

This would suggest that China’s production has not been relocated to other Asian economies because of the US tariff hike, but that somehow its exports have found an indirect way into the US. During the trade war, businesses were obviously eager to find loopholes to avoid exorbitant tariffs without having to shift production, in particular by using transshipment, in which Chinese exports are minimally processed during a brief stop at a third port and then reexported as a non-Chinese product. The US authorities have recognized and tried to reduce this practice, but apparently without much success. Several arguments would support this view: (i) despite a drop in Chinese exports to the US of $87 billion in 2019 and another $16 billion in 2020, China’s total exports to the world grew by $13 billion in 2019 and another $92 billion in 2020; (ii) the structure of China’s exports in terms of main products has remained broadly unchanged from 2018 to 2019, not displaying large disruptions following the trade war (according to the Observatory of Economic Complexity [OEC]); and (iii) the reorientation of US imports from China to other Asian economies took place very quickly, in a matter of months rather than years, when it would be almost impossible to shift production facilities so quickly from one country to another. It would also be naïve to think that much smaller Asian economies such as Vietnam could replace China as the world’s manufacturing hub overnight. China still enjoys a large comparative advantage in terms of workforce size and qualification, infrastructure, business environment, and internal market capacity.

If some production offshoring from China to low-cost Asian economies took place, it was mainly for low-tech and low-value goods, and has not affected China’s production and exports much. Manufacturing output continued growing by almost 6 percent in 2019 and 4 percent in 2020, while high-tech manufacturing advanced even faster, by 9 percent in 2019 and more than 7 percent in 2020. And although China’s trade surplus with the US shrunk by $108 billion, its surplus with all its trade partners actually increased by more than $180 billion from 2018 to 2020 (graph 3). This trend strengthened further during the first four months of 2021, when China’s exports grew on average by 40 percent from a year before and the trade surplus increased almost three times, to $160 billion. The negative economic impact of strict lockdowns and massive growth stimuli in the US and other advanced economies has undoubtedly contributed to China’s brisk export recovery since the summer of 2020. This also brings us to the heart of the problem of the US’s large and persistent current account deficits.

Graph 3: Chinese Trade Surplus with the US and the World, 2000–20

Source: US Census Bureau and UN Comtrade Database

Monetary and Fiscal Expansion Cause the US Trade Deficit

It is actually not bad that private businesses found ways to circumvent Trump’s protectionist measures. Austrian economists have always made a strong case against external tariffs, which only favor special interest groups while harming the rest of the community. Industries protected from foreign competition are subsidized by domestic consumers and other producers, who see their sales and export markets shrink. Overall, import restrictions do not increase domestic employment or real wages, but do change the structure of production for the benefit of less efficient businesses, both domestic and foreign. Hazlitt noted that “a tariff is not irrelevant to the question of wages. In the long run it always reduces real wages, because it reduces efficiency, production and wealth.”

Murray N. Rothbard criticized protectionist arguments, which were primarily directed at Japan in his days. He also claimed that “in the fiat-money era, balance-of-payments deficits are truly meaningless” because they do not trigger gold outflows. Deficits are fully covered by foreigners who invest the dollars acquired with their exports in American assets and debt instruments. Other Austrian economists have more nuanced views about the consequences of the US trade deficits. Joseph T. Salerno rejected the neomercantilist hysteria over US trade deficits too, but stated that the federal budget deficit is the real problem because it diverts foreign capital inflows from productive investment to inefficient government spending. Mark Thornton considered that the US expansionary policies were causing continuous trade deficits and that Trump’s fiscal relaxation could only worsen the situation. He concluded that the dollar’s world reserve currency status has ruined fiscal responsibility and advocated a return to the classical gold standard as the only way to fix the chronic US trade deficit.

Indeed, data shows that monetary creation accelerated notably after the US abandoned the gold standard in 1971, and that soon thereafter the current account (CA) balance turned consistently negative (graph 4). Moreover, the yearly fluctuations of the CA deficit have largely mirrored the annual changes in the money supply (M3). Accelerated monetary creation in the late 1970s and early 1980s, and then again in several rounds since the late 1990s, correlates well with both a widening of the CA deficit and an intensification of business cycles.

Graph 4: US Current Account Balance and M3 Money Supply, 1961–2021

Source: Federal Reserve Economic Data (FRED).

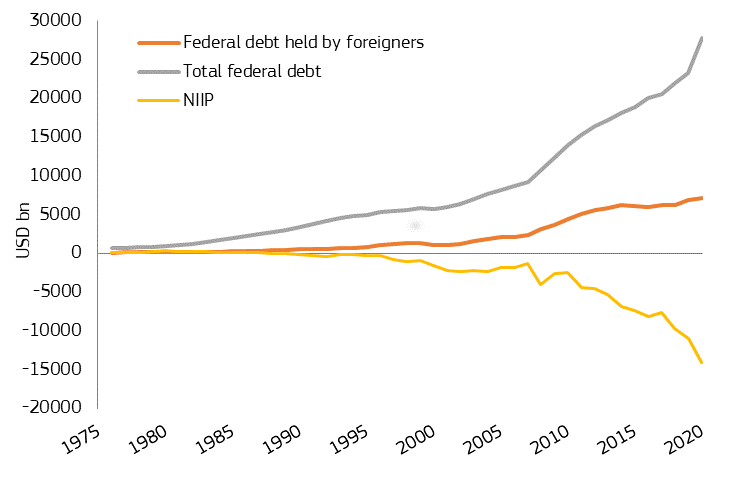

A similar link can be seen between the massive increase in federal debt and a growing negative US net international investment position (NIIP)3 (graph 5). Since the 1970s, the US has gradually turned from the world’s largest net creditor into its largest net debtor, with NIIP peaking at about $14 trillion, or 66 percent of GDP, in 2020. Total public debt rose to almost double this amount and its part held by foreign investors exceeded $7 trillion in 2020. Foreign-held public debt was modest, at about 5 percent of total public debt during the gold standard, but surged above 30 percent of the total since 2010 and also doubled its share to about 20 percent of total US foreign liabilities during the last two decades. Overall, foreign dollar inflows that finance public spending rather than bolster private capital accumulation have been on the rise.

Graph 5: Total US Federal Debt, Foreign-Held Debt, and NIIP, 1975–2020

Source: FRED.

The US dollar’s status as the world’s main reserve currency is only a blessing in disguise, because it removes several constraints on implementing expansionary macroeconomic policies. First, with the severing of the US dollar’s link to gold, the ability to keep in check not only the trade deficit, but also the artificial credit expansion of fractional reserve banks, via gold outflows, has been lost. Second, in the case of ordinary fiat currencies, excessive credit expansion and trade deficits trigger a depreciation of the currency, pushing up domestic prices and pressuring the central bank into raising interest rates and reducing credit growth. As the world’s main reserve currency, the dollar is partially shielded from this correction mechanism and kept artificially strong. Third, low interest rates and increased external demand for US government securities facilitate larger fiscal deficits financed by monetary expansion.

Even if the US trade deficits were fully financed with dollars that return as capital inflows to the US economy, they could still be harmful, because the dollar’s “exorbitant privilege” enables excessive money printing and artificially low interest rates. According to the Austrian theory of the business cycle (ABCT), this causes recurrent booms and busts, malinvestment, and overconsumption. Together with higher budget deficits, the latter impact capital accumulation and productivity growth negatively. What may seem an advantage of receiving free gifts from foreigners may actually be a sure recipe for oversized government, overindebtedness, and a gradual erosion of the structure of production. At the same time, if the US policy stance becomes too expansionary relative to the one of its external partners, a loss of confidence in the dollar could threaten its special status. But as long as geopolitical factors continue to play an important role and the US is able to “export” its policy stance to the rest of the world, only a significant worsening of economic conditions could change the status quo.

Conclusions

President Trump’s protectionist trade measures against China and other external partners have not caused a reduction of the total US trade deficit. The latter actually grew further as China’s exports found indirect ways into the US and massive domestic growth stimuli were deployed during the pandemic.

The chronic US trade deficit is a direct result of the dollar’s status as the world’s main reserve currency and unabated monetary and fiscal expansion. Resorting to protectionism to solve the US trade deficit is both useless and harmful due to the additional economic distortions it entails.

- 1. The protectionist stance went beyond China as the Trump administration increased tariffs for steel, aluminum, and solar panels for almost all trade partners, renegotiated the North American Free Trade Agreement (NAFTA) with Mexico and Canada, made new trade deals with Japan and Korea, and withdrew from the Trans-Pacific Partnership.

- 2. Both Chinese and US exports to Hong Kong shrank because of the latter’s political and economic turmoil.

- 3. The NIIP measures a country’s financial position relative to the world and is given by the sum of current account balances and changes in the market value of foreign assets and liabilities.